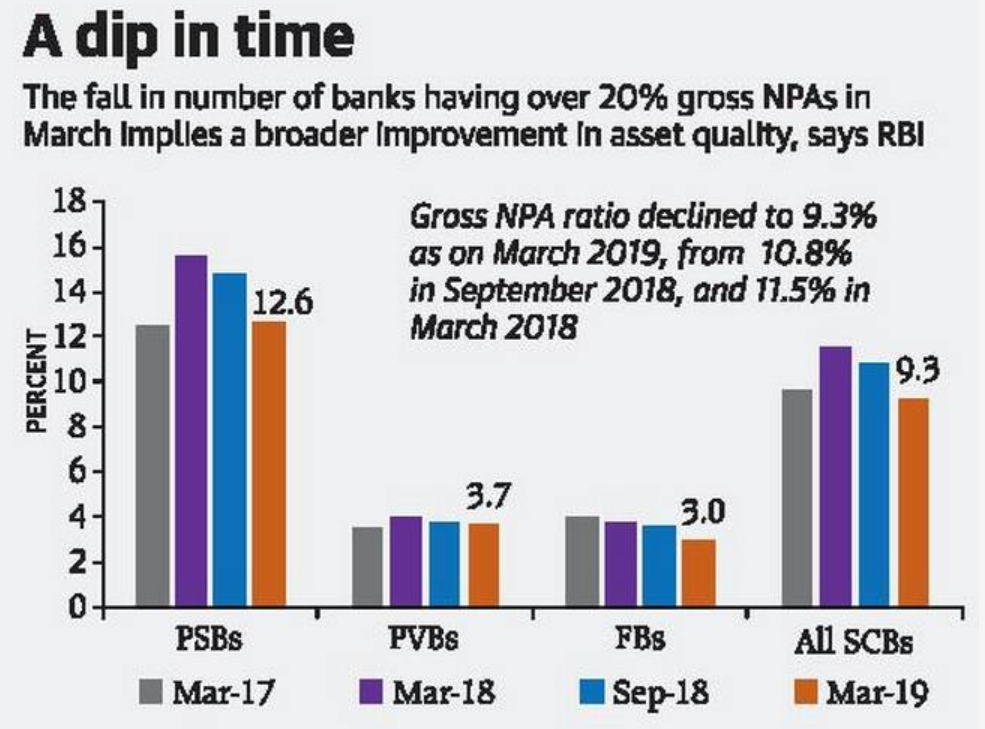

Gross non-performing assets (GNPA) in the banking system have declined for the second consecutive half year, while credit growth is picking up, the Reserve Bank of India (RBI) said in the half-yearly Financial Stability report. Gross NPA ratio declined to 9.3% as of March 2019. It was 10.8% in September 2018 and 11.5% in March 2018.

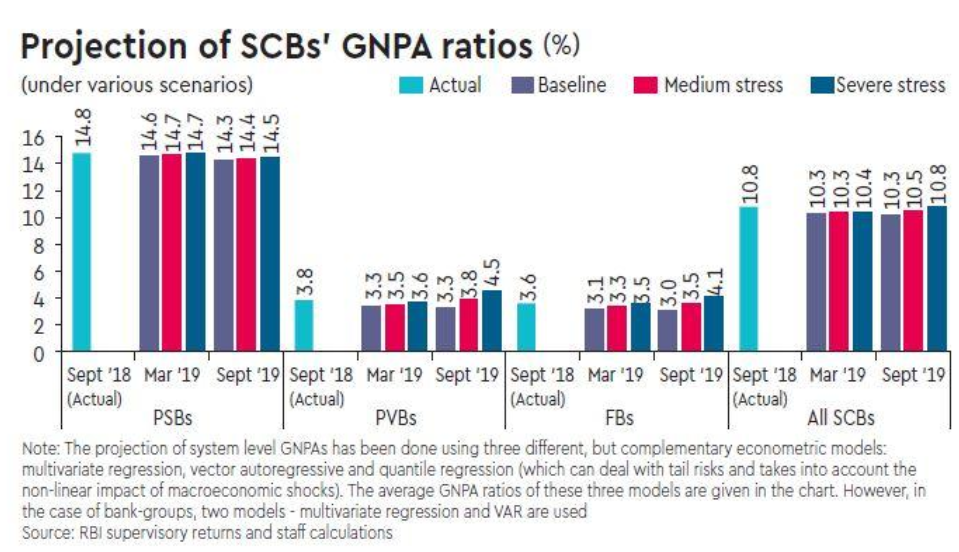

Above GNPA was much below from what RBI has anticipated a fall to 10.3% by March 2019. GNPA could further decline to 9% by March 2020, the macro stress tests indicated.

Earlier, Bad loan recognition accelerated largely due to a nudge from the Reserve Bank, which wanted bank balance sheets to reflect a true picture of the stress. The RBI’s asset quality review led to a massive spike in NPAs, and was supported with the enactment of the bankruptcy law for resolving the cases. However, the progress on the bankruptcy cases has not been very fast as the legal provisions keep getting challenged frequently and the lack of precedents results in delays in arriving at resolutions due to legal tangles.

Various Internal & External factors contribute to Increase in NPA in the banking system.

External Factors:-

a) Bankruptcy law still not effective b) Ineffective recovery tribunal c) Willful Defaults d) Natural calamities e) Industrial Sickness f) Lack in Demand g) Change in Govt Policies

Internal Factors:-

a) Defective lending Process b) Inappropriate Technology c) Improper Swot analysis d) Managerial deficiencies e) Poor credit appraisal system f) Absence of regular industrial visit

Indian Banks has to focus on the above issues to substantially bring down NPA’s in the coming future.

Big Question…Is it right time to invest?

The revival of Indian Economy is not possible without the participation of the banking sector. Banking stocks are having the highest Market capitalization in Nifty Index & BSE Index. In the near term, for the private banking space, competition landscape has become better. NBFCs have become weaker and PSU banks are slowly reviving. The woes of asset quality are behind the large private sector banks. They don’t have a dearth of capital and this has helped the run-up in the banking segment.

Again due to the NBFC crisis, few private & public banks were able to grab up this high quality selected lending books from NBFC.

One can go for long term horizon with private banks & very selective public sector banks.

Happy Investing !!!

CA Tapan Doshi – (M) 919726483113, Email id-tapydoshi@gmail.com

Investor Advisor – Stock Broker – Kotak Securities Franchise